East Africa is on the brink of an energy boom, driven by major oil and gas discoveries in Uganda, Kenya and Tanzania. These reserves are rapidly transforming the region’s investment landscape.

In 2025/26, these countries are ramping up production, deepening exploration, and building infrastructure to meet rising global energy demand.

East Africa is now more than a scenic destination, it’s a high-potential frontier market for energy investors.

From crude oil fields in Uganda’s Albertine Graben to natural gas offshore Tanzania, the region offers compelling prospects for those seeking long-term returns in the oil and gas sector.

A Surge in Global Demand Meets Regional Potential

East Africa’s strategic location and untapped reserves have attracted major global players. As energy demands continue to surge globally, especially in Asia and Europe, investors are looking to the region to bridge supply gaps.

According to the International Energy Agency, the demand for oil and gas will remain strong through 2030, even amid the green energy transition.

In response, countries like Uganda are moving fast. Uganda’s confirmed reserves of over 6.5 billion barrels of crude oil have drawn heavyweights like TotalEnergies and the China National Offshore Oil Corporation (CNOOC).

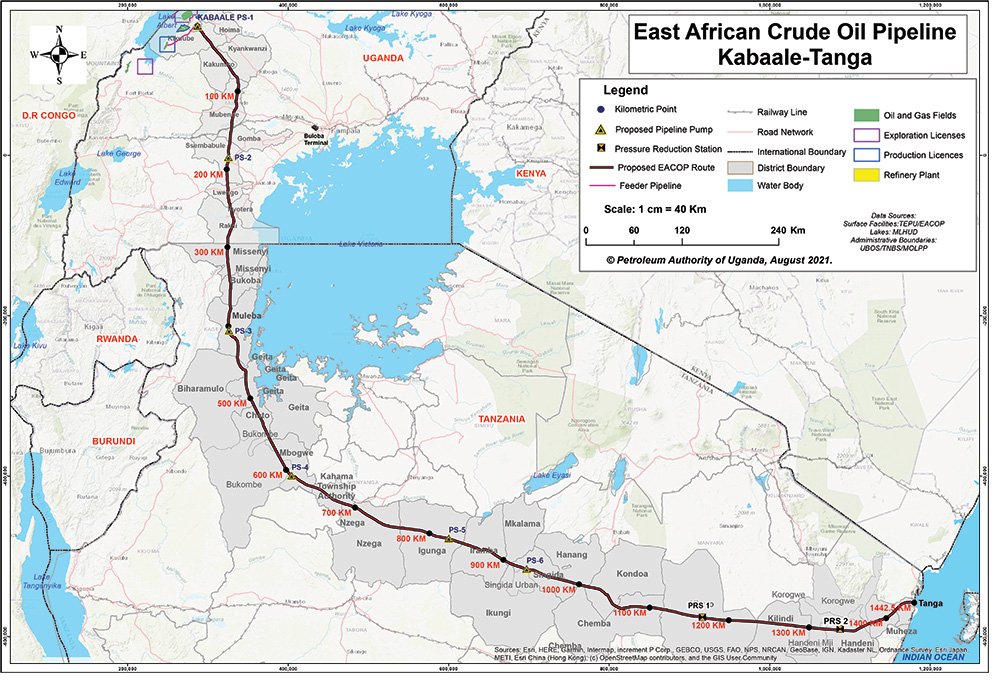

The upcoming East African Crude Oil Pipeline (EACOP) is expected to export up to 216,000 barrels per day once completed, positioning Uganda as a key regional exporter.

Uganda: Laying the Foundations for Export

Uganda’s oil and gas sector has gained global attention with the development of the Lake Albert oil fields.

Commercial production is slated to begin by 2025, supported by infrastructure such as the EACOP and a planned refinery in Hoima.

French energy giant TotalEnergies has already invested over $10 billion in Uganda’s upstream operations and the pipeline project.

The government has also introduced competitive licensing rounds, local content policies, and tax incentives aimed at creating an investor-friendly environment.

The Petroleum Authority of Uganda (PAU) oversees the sector’s regulation, ensuring transparency and compliance with international best practices.

These efforts are already paying off. For example, the Kingfisher oil field, operated by CNOOC, recently completed drilling of its first production well, a major milestone toward Uganda’s oil production ambitions.

Tanzania: Gas Reserves Set the Stage for LNG Leadership

Tanzania has emerged as a regional gas powerhouse, boasting over 57 trillion cubic feet of proven natural gas reserves, mainly offshore in the Indian Ocean.

Major companies such as Shell and Equinor are leading exploration efforts, supported by government plans to develop a $42 billion Liquefied Natural Gas (LNG) export terminal in Lindi.

The LNG project, which is in advanced negotiations, could position Tanzania as a major global gas supplier.

In parallel, the Tanzania Petroleum Development Corporation (TPDC) is working with smaller partners to expand domestic gas networks for industrial and urban use.

Tanzania’s strategic vision is to use gas to power both its economy and export market. By balancing domestic industrialization goals with international partnerships, the country is offering opportunities in infrastructure development, logistics, and downstream services.

Kenya: From Discovery to Commercialization

Kenya, though newer to the oil scene, has made strides since the discovery of commercial oil in Turkana County by Tullow Oil in 2012.

With an estimated 560 million recoverable barrels, Kenya is working to commercialize its reserves through the South Lokichar Basin project.

The government has proposed the development of the Lokichar–Lamu crude oil pipeline to facilitate exports via the Lamu Port. While investment delays and regulatory uncertainty have slowed progress, renewed interest from regional and Chinese investors could reignite momentum in 2025.

The Kenyan government has also introduced new fiscal and environmental regulations aimed at encouraging sustainable oil development. In the meantime, early oil pilot schemes have demonstrated viability, exporting small batches to international markets.

Technology Redefining Exploration and Production

Technology is playing a transformative role in East Africa’s oil and gas development. The adoption of digital tools, such as seismic imaging, artificial intelligence (AI), and big data analytics, has improved exploration accuracy and operational efficiency.

In Uganda, TotalEnergies is using advanced geophysical surveys and horizontal drilling techniques to reduce surface disruption and maximize well output.

Hydraulic fracturing and directional drilling have also enabled access to previously unreachable reserves, making even marginal fields commercially viable.

Meanwhile, innovations in remote monitoring are helping to cut operational costs and improve safety across sites in Uganda and Tanzania.

Renewable integration is becoming more common, too. Companies are beginning to use solar energy to power rigs or reduce reliance on diesel generators.

In the long run, hybrid oil-renewable models could help companies in the region lower emissions and align with global ESG standards.

Incentives Driving Investment in Uganda

Uganda is positioning itself as one of the most attractive investment destinations in Africa’s oil sector.

The government offers tax exemptions on imported oil equipment, reduced royalty rates, and investment protection guarantees.

More importantly, Uganda has committed to transparency through its participation in the Extractive Industries Transparency Initiative (EITI), reinforcing investor confidence.

The PAU’s clear regulatory framework and streamlined licensing process are designed to reduce bureaucratic delays and encourage foreign direct investment.

Local content requirements also ensure that Ugandans benefit directly from oil activities, with jobs and contracts reserved for local companies.

This is especially evident in the Tilenga and Kingfisher projects, where Ugandan firms are involved in logistics, catering, and construction.

Environmental Sustainability at the Forefront

Sustainability is a growing concern as oil production nears. Governments and companies in East Africa are increasingly under pressure to balance economic ambitions with environmental protection.

The EACOP project, for instance, has faced global scrutiny over its environmental impact, prompting TotalEnergies and the Ugandan government to strengthen environmental and social safeguards.

Companies are adopting best practices in environmental management, including environmental impact assessments, spill prevention measures, and carbon mitigation strategies. In Tanzania,

Shell has committed to carbon-neutral LNG operations, while Uganda is exploring carbon capture technologies in collaboration with international partners.

The integration of renewables and clean energy offsets within oil operations is becoming more common, aligning with global sustainability goals and reducing long-term environmental risks.

Key Players in the Region’s Energy Landscape

TotalEnergies and CNOOC dominate the East African upstream landscape, but regional companies are also emerging as important contributors. Kenya’s National Oil Corporation and Tanzania’s TPDC are increasingly involved in upstream and midstream projects, ensuring that national interests are safeguarded and local capacity is developed.

Joint ventures between African and foreign firms are also on the rise. For example, Uganda’s National Oil Company is partnering with international firms to develop refinery and petrochemical facilities, while Kenyan contractors are involved in feasibility studies for the Lokichar–Lamu pipeline.

These partnerships provide a win-win opportunity: international expertise meets local knowledge, creating sustainable and scalable projects.

Challenges to Watch

Despite the optimism, the region’s oil and gas sector faces real challenges. Political instability, infrastructure gaps, land disputes, and financing delays can derail projects.

For instance, community resistance in Uganda and legal hurdles in Kenya have slowed project timelines.

Infrastructure remains a bottleneck. With few refineries and limited pipelines, countries must invest in transport and processing facilities to make large-scale production viable. Without these, oil may remain stranded, and returns delayed.

Social and environmental opposition, especially from international watchdogs can also pose reputational risks to investors, underscoring the need for transparency and local engagement from the start.

Outlook for 2025/26: A Region on the Rise

Looking ahead to 2025/26, East Africa’s oil and gas sector is set for significant milestones. Uganda is expected to begin commercial production, Tanzania may break ground on its LNG export terminal, and Kenya could revive its stalled pipeline project with renewed funding.

The broader outlook is defined by strategic partnerships, stronger regulation, and sustainable practices. As global demand persists and technologies evolve, East Africa could become a major contributor to the global energy mix.

Now is the time for investors, entrepreneurs, and governments to align on a shared vision for energy-driven development.

With the right investments and safeguards, East Africa’s oil and gas industry can fuel not only regional growth but also shared prosperity for generations to come.