As mobile money becomes a central part of Uganda’s financial ecosystem, a new challenge has emerged: unregulated digital lending and mobile wallet overdrafts that leave users financially vulnerable.

The growing culture of borrowing through platforms like Airtel Money, MTN MoMo, and other third-party apps is shaping not just personal finance but the broader economic landscape.

The Rise of Mobile Lending in Uganda

Over the past decade, mobile money has revolutionized financial services in Uganda, bringing basic banking to millions of previously unbanked citizens.

According to the Uganda Communications Commission (UCC), mobile money subscriptions surpassed 38 million by 2024, with MTN and Airtel dominating the market.

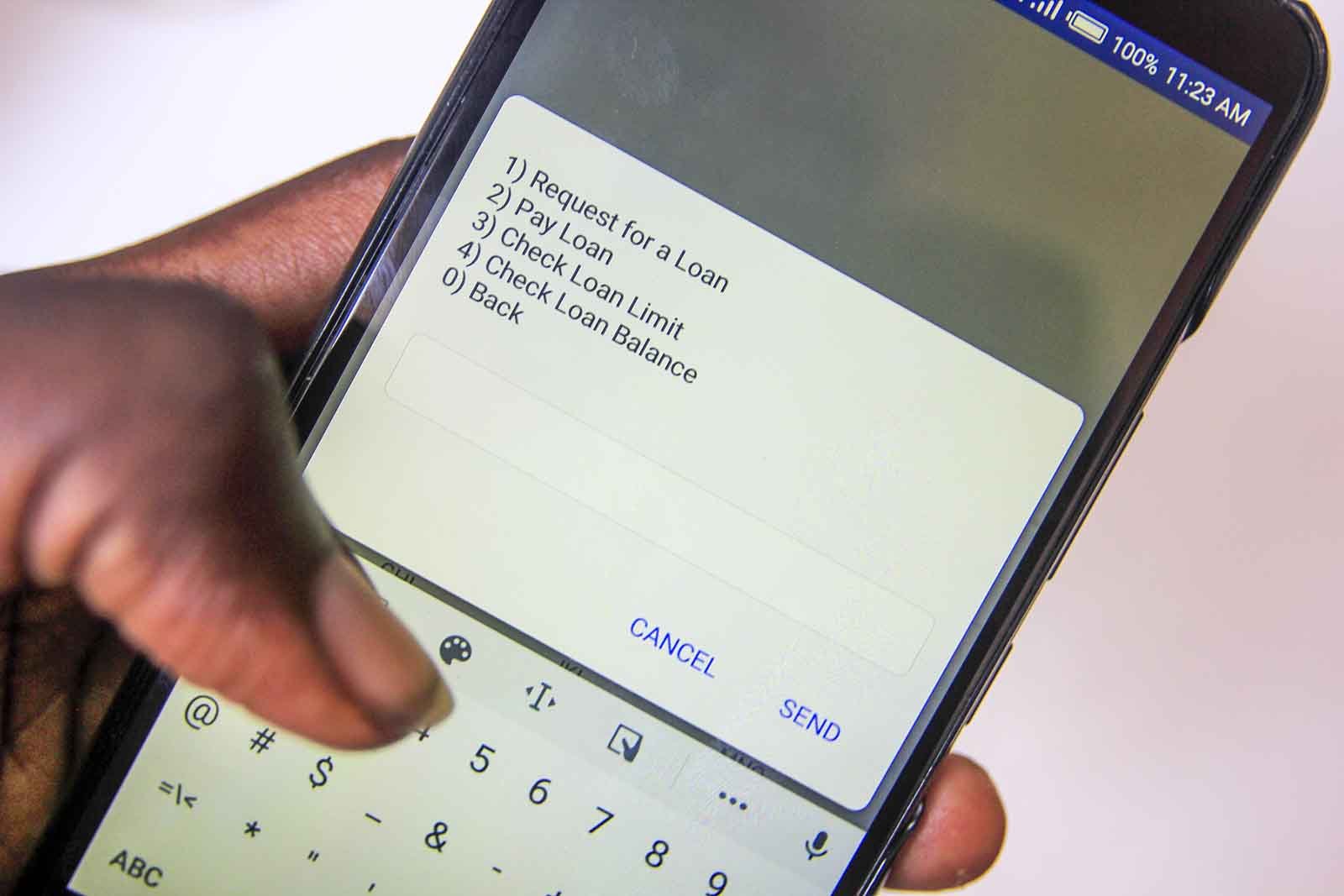

With this growth came a rise in mobile lending, particularly nano-loans, small, short-term loans offered instantly through mobile wallets.

Airtel’s Wewole, MTN’s MoKash, and the increased mobile loan Apps, such as QuicksenteOKLoan, Numida, among others, have made it easy for users to borrow money within minutes, often without formal credit checks or paperwork; however, this convenience has come at a cost.

Digital Convenience Meets Financial Pressure

Many Ugandans now face automatic deductions from their mobile money accounts the moment funds are deposited, money meant for school fees, food, or business is instead swept away by overdue loan payments.

It is not uncommon to hear phrases like “MTN already ate my money” or “Airtel deducted everything,” especially at the end of the month.

This situation has turned once-trusted mobile wallets into financial traps for some. Culprits requesting to pick up money in person to avoid losing it to deductions is both humorous and tragic, reflecting how debt has become deeply embedded in daily financial life.

The Mobile Loan Trap: Easy In, Hard Out

Most mobile loans are marketed as a lifeline during emergencies. But in reality, they often come with high interest rates, short repayment periods, and little financial literacy support.

Users borrow for airtime and emergency purchases, then default, only to be trapped in a cycle of borrowing again to cover previous loans.

According to a 2023 report by Financial Sector Deepening Uganda (FSDU), over 45% of digital borrowers in Uganda had taken multiple loans within a month, with many reporting stress and reduced savings due to continuous borrowing.

This behaviour, often described as loan stacking, indicates a deeper problem of financial instability and digital credit dependency.

Financial Inclusion or Exclusion?

While mobile lending was intended to boost financial inclusion, it is now raising concerns about digital financial exclusion.

Borrowers with poor repayment histories can find themselves blacklisted, unable to access future credit and even basic services linked to their mobile wallets.

Additionally, there is limited regulation around digital loans. Unlike commercial banks, many mobile lenders operate in a legal grey area, often escaping the strict consumer protection rules that govern formal financial institutions.

It is well known that financial inclusion without financial protection is dangerous. While millions now have access to digital loans, few have access to debt management tools, credit counselling, and savings education.

What Can Be Done?

The Bank of Uganda, in partnership with the Uganda Microfinance Regulatory Authority (UMRA), needs to enforce clear guidelines for mobile lending platforms, limiting exploitative interest rates, enhancing transparency, and requiring borrower consent before deductions.

There is a growing need for nationwide financial education campaigns, especially targeting youth, boda boda riders, market vendors, and casual workers who are most vulnerable to digital debt. Campaigns could be spearheaded by telecom companies.

Innovations that blend credit with savings incentives, such as saving rewards and interest discounts for early repayments, could help shift behavior away from chronic borrowing toward responsible financial planning.

Uganda lacks robust support for people in financial distress. Community-based programs, digital debt helplines, or even chatbots that offer budgeting tips and repayment strategies can go a long way in promoting financial wellness.

Business Opportunities Amid the Debt Crisis

Interestingly, this financial challenge also presents new business opportunities. Fintech startups can design apps focused on debt tracking, budgeting, and savings automation.

Telecoms could offer “safe wallets” where users can store funds temporarily shielded from automatic loan deductions.

Banks and microfinance institutions could also develop credit-building products that help digital borrowers transition to safer, longer-term financial services with better terms.

A Social Reflection with an Economic Undertone

In a country where 78% of the population is under 35, and digital technology is redefining livelihoods, mobile debt is not just a financial issue; it’s a youth crisis, a tech challenge, and an economic policy concern.

It raises tough questions: Are we empowering citizens financially, or creating a generation living paycheck to paycheck digitally?

Is convenience replacing financial discipline? And is humor becoming the coping mechanism for a deeper, unspoken economic struggle?

In the end, with better policies, smarter products, and a renewed focus on digital financial literacy, Uganda can turn the tide.